finPOWER Software News

finPOWER Connect 3.01.08 Released

Thursday, 13 December 2018

We are pleased to announce the release of finPOWER Connect version 3.01.08.

To upgrade to the latest version please contact your authorised Intersoft Reseller or see the Downloads page.

Some of the highlights are:

- Deposits

- Close Account wizard now supports calculations past today (when post Maturity)

- Account Statements

- New script functionality added to hide Transactions

- Workflows

- Added ability to re-open a closed Workflow

- Credit Bureaus

- Bank Statements (Proviso); new option to use branded links in Documents

- Centrix NZ; Commercial Report updated

- Secured Signing Electronic Signatures

- Added support for "Packages"

- Added Email Template support

- Added Attachment support

- Added support for Video Confirmation, Review and to require Reason and Job Title when signing

For a full list of all the release notes click here.

finPOWER Connect 3.01.07 Released

Wednesday, 17 October 2018

We are pleased to announce the release of finPOWER Connect version 3.01.07.

To upgrade to the latest version please contact your authorised Intersoft Reseller or see the Downloads page.

Some of the highlights are:

- PPSR NZ Interface

- Organisations with an NZBN Business Type of "NZ Unlimited Company" fail to Register

- PPSR NZ Search; now supports 1,000 results (was previously limited to 300)

- PPSR NZ Update wizard; Amend action now automatically cleared if no changes have been made

- Updated functionality to support older PPSR G2B Searches

- Business Layer

- ExecuteRegister now returns a list of Pre-Validation Errors

- AccountAppFunctions and ClientFunctions, "GetLatestSecurityRegisterSearch" not returning new PPSR NZ searches

- Bank Import Services

- "ASB CAPE" import service added.

- SQL Server Databases

- Reinitialising Database Connection may error

For a full list of all the release notes click here.

Client Newsletter

Tuesday, 9 October 2018

The Finance Expo 2018 - "It's about Working Smarter"

The Finance Expo 2018 is locked in for 5th November in Christchurch, and 7th November in Auckland and has a great new look and feel, as well as an exciting line up of Presenters.

This year’s edition of The Finance Expo is themed around Working Smarter. Hear presentations from leading industry providers, a review of the PPSR replacement programme as well as the latest developments and trends in the finance industry.

If you are a member of the NZ finance industry, from Tier One lenders to the smallest Loan Company – The Finance Expo is for you. Our Presenters cover a number of highly relevant topics, and networking opportunities are provided. Then join us for lunch and an opportunity to interact with key industry providers.

For further details and to register see https://www.financeexpo.co.nz/.

A new PPSR in New Zealand

Monday, 1 October 2018

The new PPSR is here

The replacement PPSR was successfully launched on 1st October 2018.

The move was driven by the Ministry of Business Innovation and Enterprise (MBIE) and was designed to replace the reliable but aging platform that, whilst world leading when it was released in 2002, had increased risks and costs associated with ageing technology.

Clients on the older finPOWER system will need to upgrade to finPOWER Connect to use the new PPSR.

Clients using finPOWER Connect should upgrade to version 3.1.6 or later to use the new PPSR.

If you have any queries or questions, please do not hesitate to contact Paul Thompson or your Intersoft Dealer.

finPOWER Connect 3.01.06 Released

Tuesday, 25 September 2018

We are pleased to announce the release of finPOWER Connect version 3.01.06.

To upgrade to the latest version please contact your authorised Intersoft Reseller or see the Downloads page.

This release includes a few last minute tweaks for the NZ rPPSR Interface.

We only recommend you upgrade to this version if one of the following issues will affect your system:

- You use Workflows, and in particular "Register Security Statement" or "PPSR Search" type items.

- You use Page Sets, and in particular include a drilldown to the "PPSR Search" form.

For a full list of all the release notes click here.

We are pleased to announce the release of finPOWER Connect version 3.01.05.

To upgrade to the latest version please contact your authorised Intersoft Reseller or see the Downloads page.

Some of the highlights are:

- NZ rPPSR Interface

- This release includes final changes for the NZ PPSR.

- It is highly recommended all users integrating to the NZ PPSR upgrade to this version prior to the Go-Live date.

- Various enhancements and issues fixed.

- Better handling of leading whitespace and multi-line Collateral and Item descriptions.

- Updated to handle request throttling, including setting minimum Timeout to 180 seconds.

- Improved matching of Debtors.

- Various enhancements to SPG Report.

- Account form.

- Improved time required to load the form the first time opened.

- Bank Export Services.

- Added "ANZ MT101 Payments (Direct Credit)" file export.

- Added "ANZ Domestic Payment (Direct Credit)" file export.

- Added "ANZ Domestic Payment (Direct Debit)" file export.

- Credit Bureau Interfaces.

- Centrix.

- Updated service URL endpoints to v16.

- Equifax NZ.

- Added Intersoft identifier to Transaction Reference.

- HTML Widgets.

- Various improvements and fixes.

- New and enhanced Controls, including Grid, Document Manager and IconComboBox controls.

- Countries.

- Added support for United Kingdom.

For a full list of all the release notes click here.

How to Guide: Centrix Credit Report

Wednesday, 22 August 2018

The Centrix Credit Report is a very powerful tool in making lending decisions. It is a culmination of all the information Centrix has about a person as well as checking several external databases to add even more information to the dataset. With this information in your hands you can make a clear, informed decision about the risks of lending to an individual.

finPOWER Connect allows you to interface with Centrix without having to purchase any additional modules and brings the power of the Centrix Credit Report directly into finPOWER Connect. Once a Credit Report has been completed, the Report is automatically stored against the client for easy access in the future.

Centrix holds credit information on over 3.4 million New Zealanders. Comprehensive Credit Reporting (CCR) is gaining momentum, with 23 providers of data participating already. Centrix holds CCR data on 2.95 million New Zealanders, and with several more credit providers in project to participate, this number is growing fast.

Centrix Credit Reports are:

- Fast and Efficient

- Comprehensive

- Include Predictive scores

- Cost Effective

- Delivered straight to your finPOWER Connect desktop

The Recommended Retail Price for the Centrix Credit Reporting Suite are:

| Consumer Credit Report including: | |

|---|---|

| Credit File details (enquiries, defaults) Court Fines Data Property Ownership Records Companies Office Records Name Only insolvency CCR Data (if Registered) |

$6.00 plus GST |

In addition to risk assessment, Centrix can also assist with your AML requirements. Their SmartID suite of products

allows

to confirm the identity of a person by verifying their Drivers Licence or NZ Passport and a range of other information

sets.

Smart ID – Electronic ID Verification to assist meeting your AML requirements:

| Smart ID Verification, including: | |

|---|---|

| Bureau ‘trusted source’ File check (CCR, Retail Energy) Property ownership PEP/Sanctions (Thompson Reuters) |

$2.75 plus GST |

| Smart ID plus Driver Licence Verification | $2.75 plus GST |

| Smart ID plus NZ Passport Verification | $4.40 plus GST |

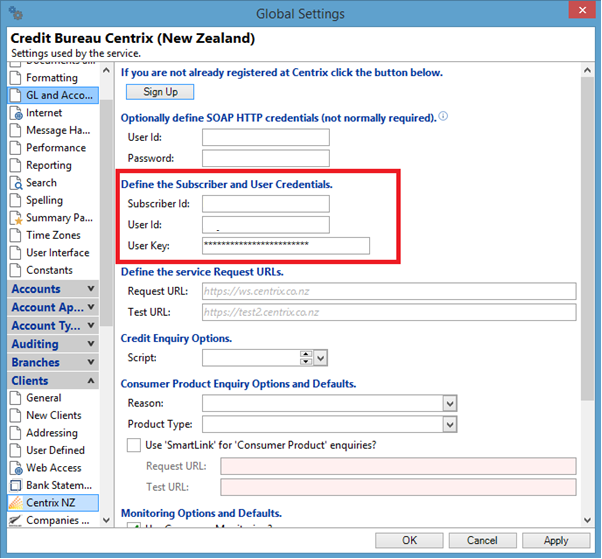

To Configure your Centrix Account

You must have a registered Centrix Account. If you do not already have an account, click here.

Once you have your Centrix Account, enter your Subscriber ID, User Id and User key into Tools, Global Settings, Clients, Centrix NZ.

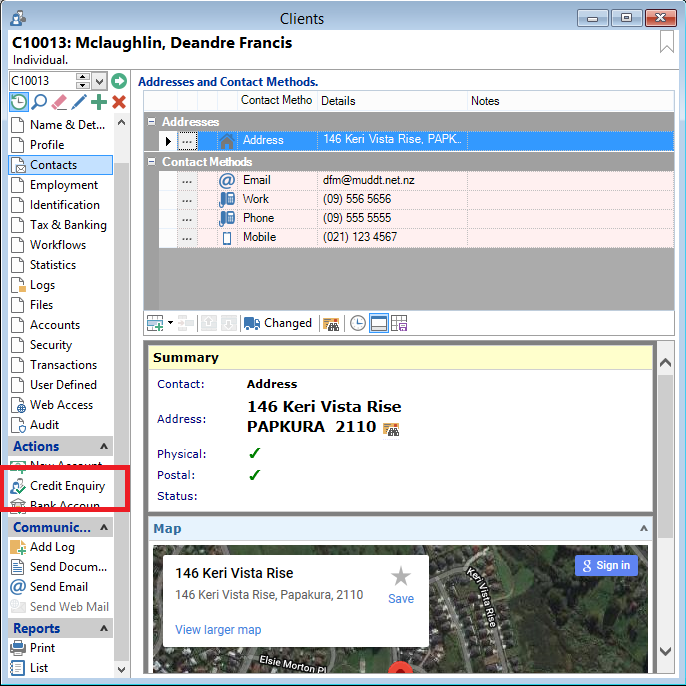

To initiate a Credit Report

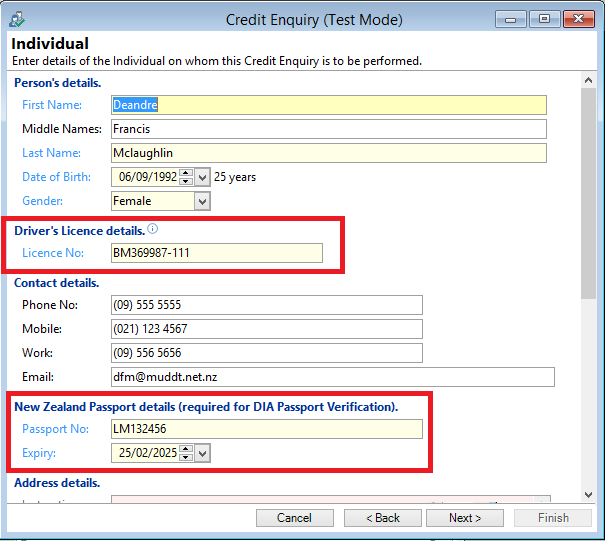

From the required Client select Credit Enquiry from the Actions Menu Bar.

Alternatively you can also access the Credit Enquiry Request Form from:

- Clients, Credit Enquiry

- Workflow items

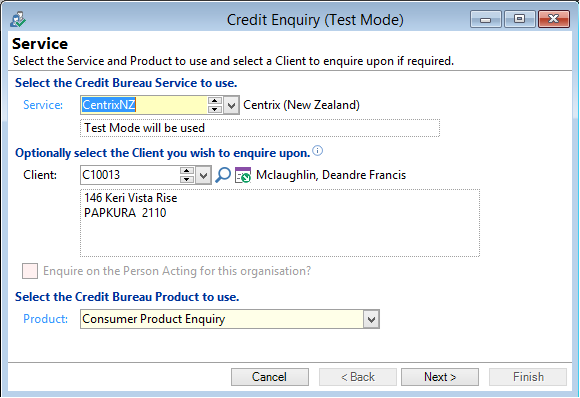

The Credit Enquiry Request Form

The Client will be defaulted if you have initiated the Credit Enquiry from the Client screen or a workflow, but it can be left blank if you want to manually enter to individual’s details.

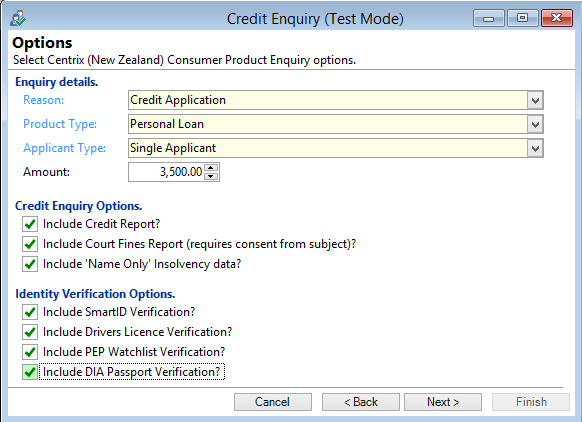

From the Credit Enquiry Options, select the information you want to see on the Report.

- Include Credit Enquiry includes the standard Centrix Credit Report

- Include Court Fines Report includes any paid or outstanding Court fines the individual may have

- Include Name Only Insolvency data includes a check against Insolvency Records using only the Client's Name

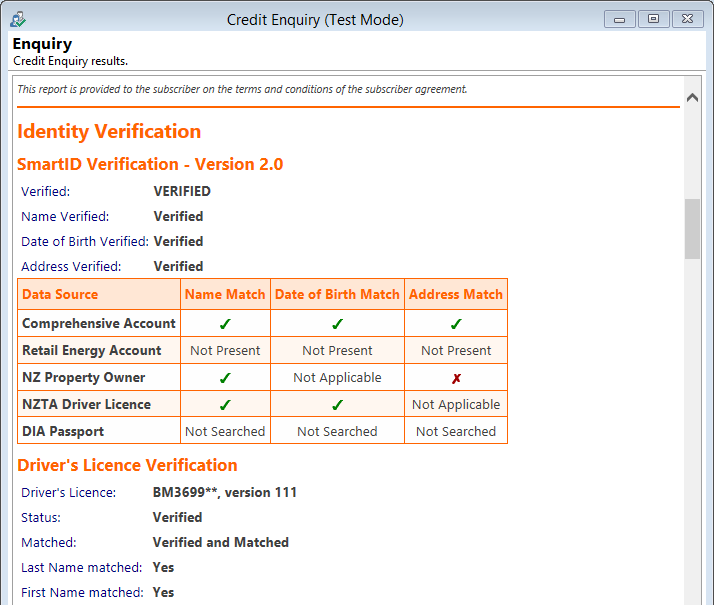

If you want to verify the individual's identity using the Smart ID service from Centrix, select the required options:

- SmartID Verification includes:

- Bureau 'trusted source' File check (CCR, Retail Energy)

- Property ownership

- PEP/Sanctions (Thompson Reuters)

- Driver Licence Verification allows you to check the entered Drivers Licence details against the NZTA database

- PEP Watchlist Verification check the individual against the PEP (Politically Exposed Persons) register

- DIA Passport Verification checks the supplied NZ Passport details against the DIA (NZ Department of Internal Affairs) database

Click Next and enter the relevant details if they have not already been completed. The Drivers Licence and Passport details will be pre filled from information you have previously entered into the Identification Page on the Client file.

Note; you would generally only select one of Driver Licence or Passport Verification.

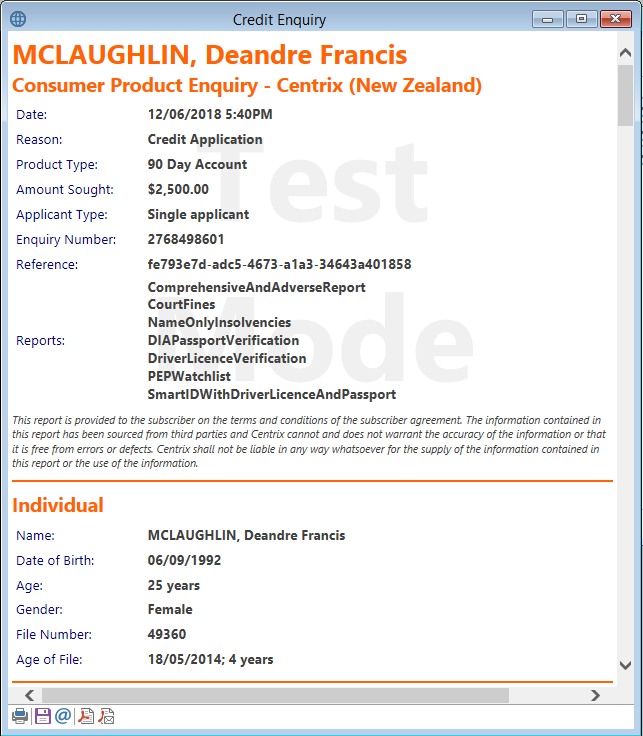

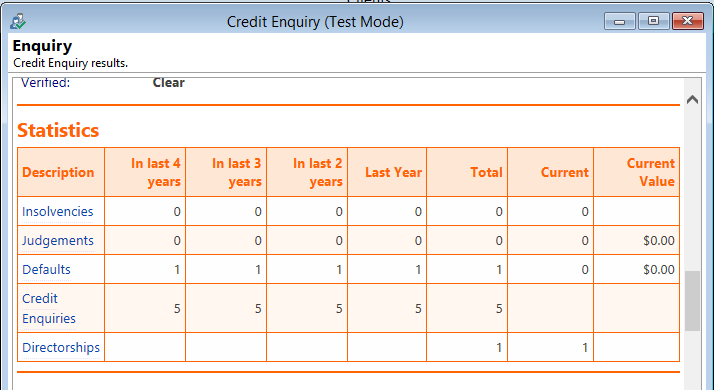

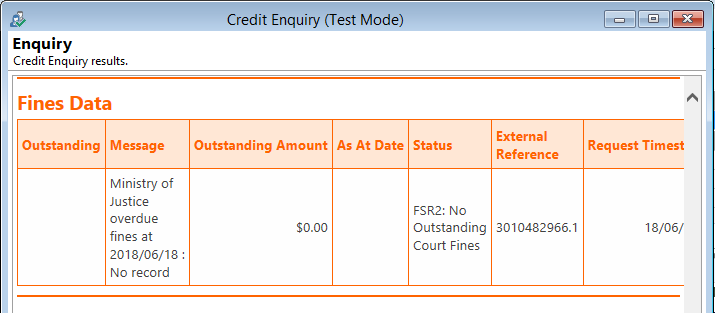

The Credit Report Explained

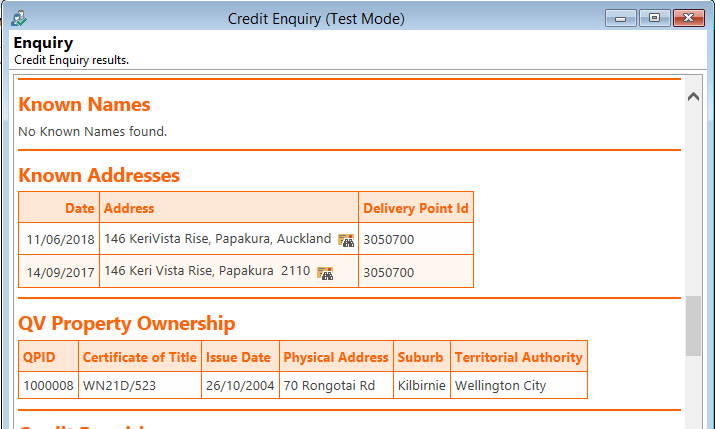

The first section of the credit report confirms the details you submitted and lists the reports that go to make up the Credit Report. It also confirms the Client’s details and the age of the File (how long Centrix has had a file on the individual).

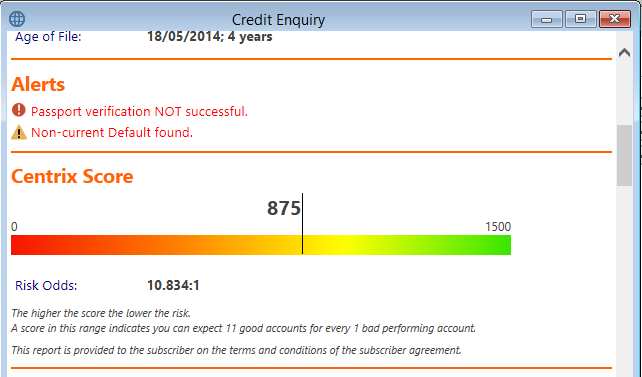

The Risk Odds score is a measure of what is the likelihood of an account for this client going bad. In the example below there is a 1 in 11 chance of an account going bad – obviously the higher the Risk Odds Score the better.

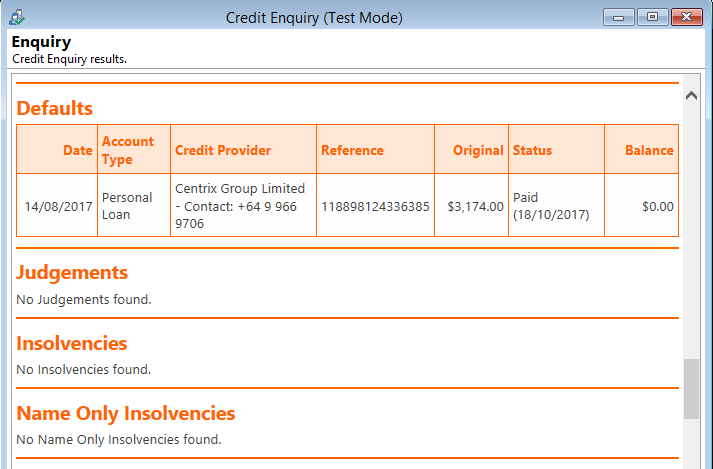

Any defaults loaded on the Bureau are detailed including Defaults that have been fully paid. Specific details on negative Credit Data are provided as well.

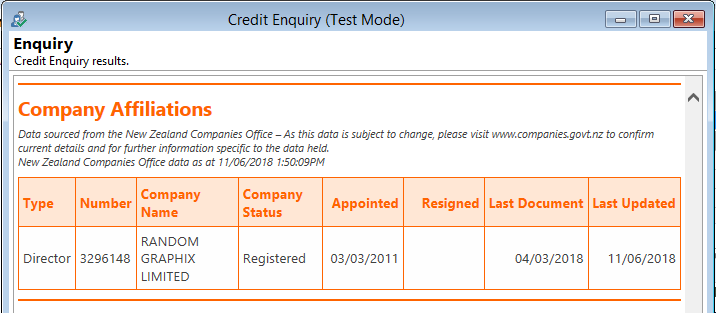

If the individual is associated with any companies, either as a Director or Shareholder, Centrix interrogates the Companies office and reports the information back in the Credit Report.

Likewise, any Court Fines are investigated by Centrix and detailed in the Credit Report.

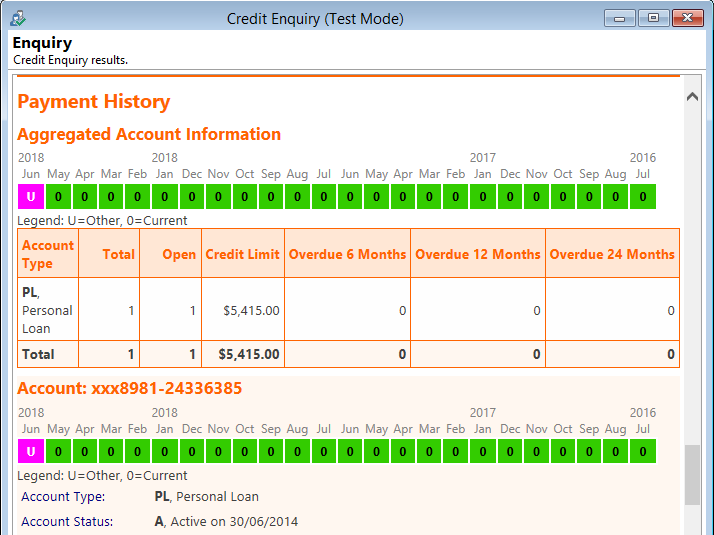

If you are registered with Centrix and are providing Comprehensive Credit Data, then your Credit Report will include the Payment History of all other loans and credit accounts supplied by other Credit Providers under the CCR framework. The Aggregated Account Information section summarises the payment history of all the Credit Accounts Centrix has CCR data on and then each Credit Account is detailed individually.

The CCR Payment History data is invaluable for providing clarity in making your lending decisions. Being able to clearly view an individual’s payment performance across a broad spectrum of lenders and utility providers allows you to better evaluate the most recent payment history for an individual and better assess their ability to repay a new loan.

Client Newsletter

Wednesday, 15 August 2018

Guidelines and Information for PPSR Go Live

As you are all no doubt aware, the new PPSR platform will be going live in just a few short weeks. In preparation, we have put together some points to note, actions to take and some suggestions to help you get ready for the rPPSR.

MBIE will close the current PPSR website and G2B interface at 5:00 pm on Friday 28th of September. The new PPSR will commence operation on Monday 1st of October.

Please note that finPOWER Connect will not automatically switch over to the rPPSR Interface. finPOWER Connect will only start using the new PPSR once the "Use the new PPSR API?" checkbox in Global Setting has been checked.

During the weekend of 29th and 30th of September, the data in the existing PPSR will be migrated to the new PPSR. During this period the PPSR will not be accessible, e.g. to register a new Financing Statement or to search the Register. For this reason, services from MotorWeb and Centrix that use the PPSR will not be available, i.e. MotorWeb Vehicle Reports and Centrix Wheels Reports will return a failure message.

Therefore, you need to carefully consider how this will affect your business and plan accordingly. For example:

- If you cannot check to see if there is a Security Interest in a Motor Vehicle, should you be trading a Motor Vehicle?

- If you cannot Register an Interest in a Motor Vehicle (or any other Collateral), should you be lending on it?

- Do any of your business processes, especially automated ones, involve a PPSR Search or a MotorWeb or Centrix Wheels check? If so, what happens if these services are unavailable and return a failure error?

Make sure you have the proper procedures in place to handle these scenarios, and do not make bad lending decisions.

MBIE Contingencies

MBIE expects no issues and have undertaken extensive testing internally and externally with vendors and stakeholders such as Intersoft Systems. However, there is always the possibility that an unforeseen complication in the data migration might occur. In this unlikely event, MBIE has a contingency to stay with the existing PPSR, i.e. the old PPSR website and G2B interface will continue on Monday.

In addition, MBIE cannot rule out an issue that means soon after the new PPSR goes live they have to revert or roll-back to the old PPSR website and G2B interface. It is very hard to determine how a scenario like this might play out, but it would be only done as a last resort. It may mean you would have to re-register Financing Statements in the old PPSR system.

To be proactive we suggest the following:

- Process Renewals whilst still using the PPSR G2B interface

- For example, during the week of 17th September, process renewals due to expire prior before 12th October.

- Avoid processing Amendments, Discharges and Renewals in the new PPSR for a period of time. We suggest one week.

- You should continue doing all Registrations and Amendments that involve a Collateral.

We will be in further contact closer to the Go Live date, but if you have any queries please contact your Intersoft Reseller.

Also, take the time to upgrade to the latest version of finPOWER Connect. We suggest you upgrade to Version 3.1.5 due to be released in the week of 27th August.

Australian Fintech Award winners

Wednesday, 8 August 2018

Australian Fintech Award winners

We are pleased to announce that one of our clients, Brighte, has won the prestigious Australian Fintech Award for Innovation in Lending.

The Australian fintech sector gathered in Sydney on the 1st of August to celebrate the 3rd Annual Australian Fintech Awards. The awards celebrate the achievements and successes of the people and businesses comprising the Australian fintech sector. The keynote speaker at the awards was The Hon. Scott Morrison MP, Treasurer, Federal Member for Cook.

The Innovation in Lending award recognises a business which offers a new or significantly improved service that implements technology to bring benefits to both lenders and borrowers. Judges were looking for innovative credit modeling, use of data elements and/or an improved user experience.

In addition to the Innovation in Lending Award, Katherine McConnell, the CEO and founder of Brighte, was awarded the Fintech Leader of the Year award which recognises an outstanding individual who has persistently contributed to the advancement of the fintech sector.

Brighte is innovating in 'no interest' consumer payment plans by streamlining processes and targeting niche segments of the market such as solar and smart home technologies. Brighte offers consumers a faster and simpler way to pay and provide vendors with a tool that will drive increased sales and assist with working capital. Brighte use finPOWER Connect in combination with their own in-house developed front end system to provide a seamless and efficient system of client onboarding, vendor transaction processing and loan management.

We congratulate Brighte and Katherine on their fantastic achievements in winning these awards and look forward to continuing to work with them in the coming years.

Client Newsletter

Thursday, 28 June 2018

Invitation to your PPSR training session

On Monday 1st of October 2018, MBIE are launching the new Personal Property Securities Register (PPSR) website.

To help you transition to the new site, they're inviting you to join them at free live training demonstrations in Auckland, Wellington or Christchurch. Alternatively, you can attend a live webinar session.

This training is targeting Users that will primarily using the PPSR website to manage their security interests, but will have some relevance for Users that will be managing their security interests through finPOWER Connect. Whilst we recommend finPOWER Connect Clients attend these, Intersoft Systems and its Dealers will have support material available that is more specific to finPOWER Connect User needs.

Free tickets to the event are available by registering online. Spaces are limited, so bookings are essential!

Click here to register now.

finPOWER Connect 3.01.04 Released

Monday, 25 June 2018

We are pleased to announce the release of finPOWER Connect version 3.01.04.

To upgrade to the latest version please contact your authorised Intersoft Reseller or see the Downloads page.

Some of the highlights are:

- Accounts.

- Account Close Quotation wizard; no longer limited to one year in advance.

- Credit Bureaus.

- Added graphical score to Equifax NZ Consumer Enquiry.

- rPPSR (New Zealand).

- Incorrectly left PPSR Transactions pending.

- Enhanced matching of Collateral.

- Various enhancements to the PPSR Transaction Report wizard.

- Documents.

- "Account Settlement Summary" Document renamed "Account Close Summary".

- Added "Account Quotation" Word Document file type.

- Added "Account Withdrawal Advice" Word Document file type.

- Added "Client Interest Advice" Word Document file type.

- Added "Account Credit Card Update" Word Document file type.

- Added "Account Tax Number Invalid" Word Document file type.

- Added "Lodgement Schedule" Word Document file type.

- HTML Widgets.

- Several system widgets added or updated.

- Centralised styling added.

For a full list of all the release notes click here.

Client Newsletter

Monday, 18 June 2018

New PPSR Go Live Date Released

MBIE has released new dates for the PPSR Go Live:

- Friday 28th September 5:00 pm, the existing PPSR will be turned off and existing data migrated.

- Monday 1st October, first business day of the new PPSR.

PPSR Customer Website Training

The scheduled Website Training Sessions, run by MBIE, will now be held:

- Wellington 9:00 am – 12:00 pm, Thursday 6th September

- Christchurch 9:00 am – 12:00 pm, Friday 7th September

- Auckland

- 1:00 pm – 4:00 pm, Wednesday 12th September

- 9:00 am – 12:00 pm, Thursday 13th September

- 9:00 am – 12:00 pm, Friday 14th September

- Webinars

- 9:00 am – 12:00 pm, Tuesday 4th September

- 1:00 pm – 4:00 pm, Wednesday 5th September

- 9:00 am – 12:00 pm, Tuesday 11th September

Invitations to these training sessions will be emailed directly to website users at the end of June.

We continue to urge all clients in the process of, or who have not yet converted to finPOWER Connect to do as soon as possible. This extra time should be seen as a buffer, not a reason for procrastination!

As always, we will keep you informed if new information comes to hand.

Client Newsletter

Monday, 11 June 2018

Centrix Client Monitoring Service

We have released a Fact Sheet and Set Up guide for the Centrix Client Monitoring service.

The Centrix Monitoring service is like having your own staff member in Centrix monitoring your clients. Each time something happens to one of your clients, Centrix sends you an email detailing the changes and alerting you to the change in your client’s status. This is great for keeping track of your clients, getting ahead of the collections process and giving you greater visibility over your client base. You can receive email notifications on a monitored client for the following events:

• New Addresses

• New Adverse data (Defaults, Insolvency and Judgements)

• New Enquiries

• New Directorships

• New Shareholdings

Centrix has information feeds from many of the major utility companies, so as soon as a client sets up a new electricity or telephone connection, you will be advised. This means you know what your clients are up to and when.

Please click here for the easy to follow Set Up Guide, however you will need to have a Centrix Account to do this. If you do not have a Centrix Account, please click here.

Client Newsletter

Tuesday, 22 May 2018

rPPSR Update

Unfortunately, as some of you will no doubt know, MBIE has delayed the go live date of the new PPSR. This was originally to be the 2nd of July, but MBIE has announced this date cannot be met.

A new date is expected to be announced on 31st of May, but they have indicated it is likely to be early in the fourth quarter 2018.

For more information see http://www.ppsr.govt.nz/cms/customer-support/news-and-public-notices/what-s-new/ppsr-go-live-date-delayed.

The scheduled PPSR training sessions have also been delayed, with no new dates being released yet.

For finPOWER Users

We are aware that many of you already have a time fame locked in for your conversion to finPOWER Connect and we would encourage you to continue to strive to meet those time frames – it just means you will have more time to acclimatise to the new system and start looking at some of the functionality and features that finPOWER Connect offers.

For finPOWER Connect Users

We have released a PPSR ready version of finPOWER Connect, version 3.01.02. this version is ready for the PPSR based on the currently released API from MBIE. However, MBIE may release updates to the PPSR which may require a new version, but we are keeping any additional changes to the system out of the new releases so it should be a relatively minor process to upgrade to it.

We will keep you informed of any new dates from MBIE as they come to hand, but in the interim, please contact me here if you have any queries.

Client Newsletter

Tuesday, 15 May 2018

Time is currently racing by and we are now just 6 weeks before the rPPSR goes live.

MBIE are taking a "Big Bang" cutover approach, so this means that the old system will stop on Friday 29th of June at 5:00pm and the new system will begin on Monday 2nd of July.

There will be NO PPSR access during the cutover weekend.

This also means other services such as MotorWeb and Centrix Wheels will not be able to access the PPSR.

finPOWER Connect Users

If you currently use finPOWER Connect, we have uploaded a finPOWER Connect rPPSR Guide to our website to assist with this transition.

Additional Information

MBIE have advised that existing Users and Organisations (and the associated Direct Debit authority) will not be migrating from the existing PPSR.

This means there will be a two week period available for Customer onboarding.

- MBIE will NOT be migrating Users and Organisation Accounts from the existing PPSR

- Organisations will start afresh with new Users and Direct Debits

All Organisation Account(s), User(s) and Direct Debit(s) must be setup during Thursday 14th to Wednesday 27th June.

MBIE Training Sessions

MBIE will be providing training sessions for Clients that use the PPSR Web User Interface. You can register for these sessions here.

However, this isn't mandatory for finPOWER Connect Users as your Registrations, Amends, Discharges and Renewals should always be completed via finPOWER Connect and NOT via the PPSR website.

finPOWER Connect 3.01.02 Released

Friday, 11 May 2018

We are pleased to announce the release of finPOWER Connect version 3.01.02.

To upgrade to this latest version please contact your authorised Intersoft Reseller or see the Downloads page.

Client Newsletter

Monday, 16 April 2018

We are less than 3 months away before the new rPPSR goes live.

The new rPPSR replaces the old PPSR G2B and is due to go live on 2nd of July. The approach the MBIE is taking is a "Big Bang" cutover so there will be no transition period or cross over time where both systems are supported.

We have been working closely with the MBIE on this project and have developed tools to make the transition as smooth as possible for you. In preparation for the rPPSR coming into effect, we have prepared an initial guide as to what you can be doing NOW to prepare yourself for the changeover, this can be found here. Please read it and start the process to make your transition as easy as possible.

Current finPOWER Users

If you are still running finPOWER 5, YOU NEED TO CONVERT to the latest version of finPOWER Connect.

finPOWER 5 WILL NOT support the rPPSR and you will be forced to use the manual web portal and incur the additional costs of doing so. Only finPOWER Connect will support the rPPSR. If you have not started the process of conversion with your Reseller, contact them NOW and get the process underway. If you have started the conversion from finPOWER 5 to finPOWER Connect, you need to finalise it. There are still a number of clients yet to complete their conversions and there are only limited resources available to undertake them.

Get in NOW before it is too late.

Current finPOWER Connect Users

If you currently use finPOWER Connect you will need to make sure you upgrade to the latest version. The new PPSR functionality will only be released for Version 3.01.02 of finPOWER Connect, so it is imperative that you make plans with your Dealer to upgrade well before the 2nd July deadline.

Get in NOW before it is too late.

Not going to use the PPSR Interface?

If you stop using the PPSR Interface you should be aware that you will lose the ability to directly interface to the PPSR from within finPOWER 5 or finPOWER Connect. However, you will be able to use the new web based interface provided by the PPSR; but you will have to manually enter all your PPSR transactions from 2nd of July 2018.

This means you will have to:

- Manually enter any new PPSR registrations, including all security details and the 17 digit VIN for any vehicles.

- This is a time-consuming task.

- Any inaccuracies may mean your priority over the security may not be enforceable.

- Existing PPSR Security interests will need to be manually amended and discharged, even if they were added using the PPSR G2B Interface.

- Manually update records with details of the security registration, if you want these to populate on documents.

You should also be aware that the cost associated with PPSR transactions are double when using the web interface. For example, a Registration costs $16.10 if done via the PPSR website versus $8.05 if done via the PPSR interface, Searches cost $2.30 versus $1.15.

Of course, if you ever choose to start using the PPSR Interface module within finPOWER Connect again you may have to spend considerable time reconciling the data in finPOWER Connect versus that loaded in the PPSR.

In short, the PPSR interface provides a fast, accurate and efficient way of making sure your PPSR Registrations are kept up-to-date.

Client Newsletter

Monday, 9 April 2018

ProvCon 2018 Auckland

The team from Proviso / BankStatements will be holding their Annual Conference in Auckland next week. This is a unique opportunity to get in front of the team and better understand the product, services they offer, and a road map of some exciting new services coming in the future.

For more information see here

Getting Ready for the new PPSR

Monday, 26 February 2018

Overview

If you weren't already aware, 2018 will see the start of a new era with the introduction of rPPSR. The rPPSR has a Go Live date of 2nd July 2018.

This move is being driven by the Ministry of Business Innovation and Enterprise (MBIE) and is designed to replace the reliable but aging platform that was released in 2002.

Just like the current PPSR, the rPPSR has Organisations, e.g. Finance Companies, and within each Organisation, Users that can log in and register Financing Statements etc.

It is important you prepare for the rPPSR now to make it easier for the changeover to the new system.

Glossary

RealMe Login

The "login" you use to access various NZ Government and other businesses to prove who you are when you're online and to log into their services. For more information see https://www.realme.govt.nz/.

rPPSR

The Replacement PPSR system, i.e. the new system for maintaining Financing Statements under the PPSA.

rPPSR Organisation

A Customer Account for an Organisation processing transactions under the PPSR.

rPPSR User

A User within an rPPSR Organisation that can login and process transactions on behalf of the rPPSR Organisation.

finPOWER Connect User

A User within the finPOWER Connect application.

STEP ONE

Update your existing PPSR and G2B Account Details

So that you don't miss out on any important information from MBIE ensure that your PPSR Account details are up-to-date. For example, that your email address is current.

For more information see https://support.api.business.govt.nz/customer/portal/articles/2927464-updating-ppsr-and-g2b-account-details. This demonstrates how to update your PPSR Customer Account and G2B User Account.

STEP TWO

To access the rPPSR you must create a rPPSR User. Each rPPSR User is linked to a RealMe Login, i.e. to login to the rPPSR you must use your RealMe Login details.

RealMe Logins are controlled by the NZ Department of Internal Affairs (DIA) and are for individuals and not Organisations.

Create RealMe Logins

For each rPPSR User, remember you should have at least two in your organisation, ensure they have a RealMe Login; and if not create one.

See https://www.realme.govt.nz/what-it-is/ for more information about what it is and creating a RealMe Login.

Note: You will need to agree to the RealMe Terms & Conditions, https://www.realme.govt.nz/terms-use/realme-terms-use/ provided by the Department of Internal Affairs (DIA), specifically that Email addresses and passwords are not shared.

RealMe Logins are used to prove who you are when you're online, and to log into lots of New Zealand sites and services, like Passports, Work and Income and the Companies Office.

STEP THREE

This step includes configuring the NZBN service, which is a sister service to the rPPSR. Subscribing to the NZBN service is very similar to the rPPSR and will be used in step 5 below. In addition, you can use the NZBN Register within finPOWER Connect now.

This also confirms that your RealMe Login is working as expected and familiarises you with the processes involved.

Subscribing to the MBIE Business API

Note, this must be done for each RealMe Login you will be using.

- Go to https://api.business.govt.nz/api/.

- Login with your RealMe Account.

- Go to the My Subscriptions page to access the Consumer Secret and Consumer Keys.

Configure the Consumer Secret & Consumer Keys in finPOWER Connect

To configure the API Credentials in finPOWER Connect, go to Global Settings, Clients, NZ Government and define the Consumer Key and Consumer Secret. These same credentials will be used for the rPPSR.

To use the NZBN Register interface in finPOWER Connect you must subscribe to the NZBN subscription on the MBIE's API web page.

To subscribe to the NZBN

Note, this must be done for each RealMe Login you will be using.

- Go to https://api.business.govt.nz/api/.

- Login with your RealMe Login details (if not already logged in).

- Go to the APIs page or click "Explore APIs".

- Click on the NZBN Service and then the NZBN Search.

- At the top of this page click the "Subscribe" button

- A pop-up message appears noting that the Subscription has been requested.

- Under the "My Subscriptions" page you should now see NZBN listed under Subscribed APIs as Pending.

- You should get an email to say it is pending approval, this email may also include a request to sign the API Agreement. This will need to be signed and returned.

- After a while you will get another email saying it has been granted.

If your Subscription isn't approved within 24 hours contact the API Subscription Support Centre on 0800 624 301.

To subscribe to MBIE

Note, this must be done for each RealMe Login you will be using.

- Go back to APIs, and select Ministry of Business, Innovation & Employment.

- At the top of this page click the "Subscribe" button.

- This will show up as MBIE-Echo. This should show in your "My Subscriptions" immediately without the need to be approved.

Test your Subscriptions

Once you have received confirmation that your subscriptions have been approved you can check they work within finPOWER Connect.

In finPOWER Connect go to Global Settings, Clients group, NZ Government page and click the "Verify" button.

In addition you can now use the "NZGovernment" service in Credit Enquiries and looking up Company Information.

STEP FOUR

To subscribe to the rPPSR

To use the rPPSR interface in finPOWER Connect you must subscribe to the PPSR subscription on the MBIE's API web page.

Note, this must be done for each RealMe Login you will be using.

- Go to https://api.business.govt.nz/api/.

- Login with your RealMe Login details.

- Go to the APIs page or click "Explore APIs".

- Click on the New Zealand Companies Office Personal Property Securities category and then the PPSR link (not PPSR-G2B).

- At the top of this page click the "Subscribe" button.

- A popup message appears noting that the Subscription has been requested.

- Under the My Subscriptions page you should now see PPSR listed under Subscribed APIs as Pending.

If your Subscription isn't approved within 24 hours contact the API Subscription Support Centre on 0800 624 301.

If you wish to test the rPPSR interface before the Go Live there is a "Sandbox" environment that can be used prior to the go live date. This should not be used in your production finPOWER Connect database. For more information please contact your Intersoft Dealer.

STEP FIVE

Update Organisation Clients within finPOWER Connect

If your Company creates PPSR Registrations for Non-Individual (Organisation) Clients, we suggest importing and running the NZBNCUP (Update NZBN for existing Clients) Script.

This Script is supplied with finPOWER Connect and can be imported from:

"C:\Program Files

(x86)\Intersoft\finPOWERConnect3\Templates\Sample Scripts\Script_ClientUpdateNZBN.xml".

When run, this will update the NZBN for all existing Clients (matching where the Company Incorporation Number is defined) and return a list of Clients that were unable to be updated. Note that the Script Constant UpdateClientBusinessNumber will need to be set to True for NZBN's to be updated (if left as False, only a report is generated and no changes are made to any Clients).

Also note that the Script timeout is set to 10 minutes which may not be long enough for larger databases. We recommend running the Script in small batches to confirm results (you can control how many are updated by using the MaximumClients Script Constant), and then increase the timeout as required to update the remainder of the database.

For more information please contact your Intersoft Dealer.

finPOWER Connect 3.01.00 Released

Friday, 23 February 2018

This is a major release, including updated database and many new features. Please take your time reviewing the changes before upgrading.

To upgrade to this latest version please contact your authorised Intersoft Reseller or see the Downloads page.

Some of the highlights are:

- Clients.

- New "Residency Status" added for Individual Clients.

- "MMS" Contact Method logic changed to "Show" rather than "Supports".

- Client Merge wizard; now copies addresses and contact method from both Clients, and allows them to be marked as "Current" or "Historic".

- Accounts Applications

- Can now be accepted to a "Quote" Account.

- Accounts

- New Permission Keys added to prevent User editing the Account.

- The Pool can now be defined in the New Account wizard.

- Account Transfers; new option to limit "To Account" to those Accounts with a common Client.

- Loan Accounts now have an option to "Close" Disbursement Payouts.

- Commissions

- New "Present Value (Amount Financed)" basis added to match finPOWER 5.

- Commissions now support "Interest" elements.

- Security Statements.

- Boats; added "Boat Name" field.

- Bank Export.

- HSBC Batch Payment Direct Debit/ Credit; added separately defined HSBCnet Account Number.

- Bank Account Enquiry Add-On.

- Bank Statements (Proviso).

- New data points added.

- Credit Enquiry Add-On.

- NZ Government service.

- NZBN Entity Details; updated to include additional information.

- NZCO Disqualified Directors Search; updated to include additional information.

- Change Events mailbox added. This downloads and matches changes made in the NZBN Register to Client information.

- Equifax (Veda)

- Rebrand completed.

- Vedascore Apply; special Genesis Data values now catered for.

- Dun and Bradstreet rebranded as Illion.

- Comprehensive Credit Reporting Add-On.

- Added separate "Suspend" flag for an Account.

- Document Manager Add-On.

- Files page enhancements (beta).

- Supports one level of sub-folder.

- Now shows Read-Only status and other file information.

- Security Enquiry Add-On.

- MotorWeb.

- New product "Asset Check" added. This replaces the existing VIR Report, but includes Valuation data.

- New product "Rego Check" added. This replaces the BVI report.

- New PPSR NZ Service (beta, available after new PPSR NZ goes live).

- Added "Get Vehicle Data" product.

- HTML Widgets

- New and updated Reports.

- New Account Applications Breakdown sample.

- New Workflows Breakdown sample.

- Other samples have been updated and enhanced.

- User Interface HTML Widgets.

- Can now override the built-in forms used within finPOWER Connect.

- E.g. Account Credit Limit Change and Monitor Category Change.

- New HTML Widgets:

- Account Accept/ Decline HTML widget.

- Account Suspension HTML widget.

- Account Transaction Allocation Adjustment HTML widget.

- Queues.

- Email Disclaimer added (if licensed for the Entities Add-On).

- Branches.

- Added User Defined Data.

- Reporting.

- Most Account Reports can now be grouped by "Maturity Month".

- Deposit Control Report; enhanced to split Maturity Reinvestments from Transfers.

- New "Deposit New Business Report".

- Account Exception List Report; added "First Payment Date" exception.

- Word Documents.

- New standard Bookmarks:

- AccountLog.BalanceOverdueContractual

- AccountLog.OverdueContractualBlock

- New scripting event to handle centralised custom Bookmarks.

- ISSummaryTable border helper functions updated.

- Excel Workbooks.

- ISExcel object; now supports a basic calculation engine.

- Telephone Number dialing.

- Now uses the "tel:" URL protocol which provides a better handler for VoIP calls.

- New Portals module.

- Beta release only.

- Enterprise Edition.

- Removed support for SQL Server 2005.

- SQL Server "TEXT" columns (deprecated by Microsoft) updated to "VARCHAR(MAX)" columns.

For a full list of all the release notes click here

Speckle Launches with finPOWER Connect Back End

Thursday, 15 February 2018

Speckle Launches with finPOWER Connect Back End

Australian National not-for-profit, Good Shepherd Microfinance, has made a bold move into online lending with the support of NAB to launch Speckle - a fast online cash-loan provider which offers a better alternative for people seeking small cash loans under $2,000.

With an increasingly casual workforce, the rising cost of living and low wage growth, recent research has found that one in five households in Australia have used payday loans in the past three years. To address this need, Good Shepherd Microfinance, backed by NAB, developed a product that is better for customers by keeping the fees and costs as low as possible.

Adam Mooney, CEO at Good Shepherd Microfinance, said for the first time people will be able to access a low cost alternative that is different to anything else in the market. "Speckle loans are up to 50 per cent cheaper than most other small cash loans. Most lenders charge the maximum fees allowed by law. As a not-for-profit program, Speckle is significantly cheaper for customers. It was clear that we needed a better solution for anyone who needs to use small cash loans. Speckle will enable people to access lower cost credit when they need it most." said Mr Mooney.

Building on their long-term partnership, NAB and Good Shepherd Microfinance have joined forces to develop Speckle using leading edge technology and with the help of skilled volunteers from across the bank. The partnership selected finPOWER Connect as their back end loan management system for its ease of use and fit for purpose.

Mr Paul Thompson, CEO of finPOWER said it was a rewarding experience working with the team from Good Shepherd Microfinance. "To be involved in a project where the motives are clear and beneficial has been a timely reminder of the ultimate customers and the challenges they face."

For the Speckle configuration, finPOWER Connect interacts directly with the front end originations platform to provide a fast and efficient application process. Streamlined Loan Management and collection processes are handled by finPOWER Connect as well as all management and funding reporting.

"This sort of configuration highlights the functionality and flexibility that finPOWER Connect can deliver for a client." says Mr Thompson. "finPOWER Connect interacts seamlessly with other systems and caters for any number of lending and organisational models."

For further Information about Speckle, visit http://www.speckle.com.au.

For further Information about finPOWER Connect, visit http://www.finpower.com.au or http://www.intersoft.co.nz.

Client Newsletter

Wednesday, 31 January 2018

PPSR Upgrade

You should be aware by now that the existing PPSR is being replaced with a completely new PPSR and is due to go live on 2nd July 2018.

This move is being driven by the Ministry of Business Innovation and Enterprise (MBIE) and is designed to replace the reliable but aging platform that, whilst world leading when it was released in 2002, has increased risks and costs associated with ageing technology.

finPOWER and finPOWER Connect both have interfaces to the current PPSR G2B that allow you to seamlessly register, amend and discharge Financing Statements. However, only finPOWER Connect will be updated to interface directly with the new PPSR.

We are working closely with the MBIE to ensure finPOWER Connect will work seamlessly with the new PPSR and your business will not be interrupted by the change.

Here is a quick guide of what you need to do, depending on the system you are currently using. To find out which system you are on go to Help, About.

finPOWER Users

If you currently use finPOWER you will need to upgrade to finPOWER Connect as soon as possible. It may be that you are part way though the conversion to finPOWER Connect, or that you have scheduled it in the near future, but either way we would encourage you to give the conversion the focus and resources required to ensure you are migrated well before the new PPSR comes into effect.

finPOWER Connect Users

If you currently use finPOWER Connect you will need to make sure you upgrade to the latest version. The new PPSR functionality will only be released for Version 3.01 of finPOWER Connect, so it is imperative that you make plans with your Dealer to upgrade well before the 2nd July deadline. Most Dealers have many clients to upgrade, so you will need to get in early to confirm your upgrade timetable.

Not going to use the PPSR Interface?

If you stop using the PPSR Interface you should be aware that you will lose the ability to directly interface to the PPSR from within finPOWER or finPOWER Connect. However, you will be able to use the new web based interface provided by the PPSR; but you will have to manually enter all your PPSR transactions from 2nd July 2018.

This means you will have to:

- Manually enter any new PPSR registrations, including all security details and the 17 digit VIN for any vehicles.

- This is a time-consuming task.

- Any inaccuracies may mean your priority over the security may not be enforceable.

- Existing PPSR Security interests will need to be manually amended and discharged, even if they were added using the PPSR G2B Interface.

- Manually update records in finPOWER with details of the security registration, if you want these to populate on documents.

You should also be aware that the cost associated with PPSR transactions are double when using the web interface. For example, a Registration costs $16.10 if done via the PPSR website versus $8.05 if done via the PPSR interface, Searches cost $2.30 versus $1.15.

Of course, if you ever choose to start using the PPSR Interface module within finPOWER Connect again you may have to spend considerable time reconciling the data in finPOWER Connect versus that loaded in the PPSR.

In short, the PPSR interface provides a fast, accurate and efficient way of making sure your PPSR Registrations are kept up-to-date.

We will be in contact closer to the time with detailed notes of the PPSR changes, but, in the interim, please make sure you are on the latest version of finPOWER Connect to ensure you are prepared as possible.

Client Newsletter

Wednesday, 8 November 2017

CCR to be Mandatory

The Comprehensive Credit Reporting (CCR) just received a big boost with the Australian Government announcing it will legislate for a mandatory comprehensive credit reporting regime to come into effect by the 1st of July 2018. According to the Australian Treasurer currently less than 1 per cent of credit data is being reported.

The four major banks will be the first to be required to report; they account for approximately 80 per cent of the volume of lending to households. The four major banks will be required to have 50 per cent of their credit data ready for reporting by the 1st of July 2018, increasing to 100 per cent a year later. The Government will consult further on whether to mandate additional institutions being included on a phased in basis as well as on the implementation mechanisms for this decision, including the legislation.

The Government believes its decision will lead to greater competition in lending and provide better access to finance for Australian households and small businesses.

With this clear intent, it is only a matter of time, we believe, before CCR is mandated across all lenders, and it will not be too long before NZ follows suit.

finPOWER Connect has simplified the implementation of CCR by creating a "one step" CCR export process to export your CCR data in a format that is easily consumed by your Credit Bureau. This process circumvents many months of project work and allows clients of finPOWER Connect to start enjoying the benefits of CCR much quicker. For more information on the CCR module for finPOWER Connect see finPOWER Connect Comprehensive Credit Reporting Add-On.

finPOWER Connect 3.00.10 Released

Monday, 6 November 2017

Highlights

- Note, this is a minor update, addressing a few issues found since version 3.0.9 was released.

For a full list of all the release notes click here

Avanti Finance Transforms to faster Digital Loan Process

Thursday, 26 October 2017

Avanti Finance Transforms to faster Digital Loan Process with Secured Signing's Trusted Signature Solution

Avanti Finance customers can now enjoy a faster turnaround as they can sign loan documents online using Secured Signing’s digital signature solution as part of their finPOWER Connect Loan Management system.

Avanti Finance have been providing finance solutions to its customers for over 25 years and pride themselves on helping people solve problems and grab opportunities by providing the money they need quickly and easily. With the addition of digital signing, Avanti Finance can offer an even faster solution to its customers, that is completely online. Stephen Massey, Head of Consumer for Avanti Finance says "The feedback from both Brokers and Customers has been very positive. The Secured Signing solution has allowed us to design a signing process and experience that is flexible and meets the needs of both the Broker and the Customer".

Secured Signing delivers a great alternative to traditional paper based signing. The clear advantage is improvement to the speed of transactions, especially when multiple signatures are required with signee's spread across different locations. The convenience of online signing is backed up by the security, authenticity and legal compliance that can only be achieved with personal X509 digital signature. With a clear audit log, two factor authentications and the option to include video confirmation, Secured Signing's trusted digital signature solution is legally binding and gives you added evidence that exceeds legal requirements to be sure who is behind the keyboard.

"The driver to implement digital signatures in our business was driven by our goal to speed up the turnaround time on loan origination and simplify the acceptance process; both improving the overall customer experience" Stephen Massey said. Avanti Finance identified that not having an electronic signature capability was a gap in their offering and were impressed with the simplicity and security that Secured Signing provides. Since launching digital signing of documents generated directly from finPOWER Connect, Avanti Finance have benefited from a reduction in the time that it takes for loan documents to be signed and returned from Brokers and Customers. "It is great to see customers like Avanti Finance taking full advantage of Secured Signing's comprehensive capability to embed the convenience and security of online digital signatures into their offering." says Mike Eyal, Founder and Managing Director of Secured Signing. "The Avanti Finance team are certainly meeting their customers' expectation for a quick approval process that is completely online. I'm sure they will have every success."

finPOWER Connect 3.00.09 Released

Thursday, 19 October 2017

Highlights

- Note, this is a minor update, addressing a few issues mainly with regards to Deposit Accounts and Reporting.

For a full list of all the release notes click here

Client Newsletter

Tuesday, 10 October 2017

CCR – what to do NOW to improve your CCR experience

At the recent Finance Expo and in subsequent discussions, many of our clients expressed an interest in participating in Comprehensive Credit Reporting (CCR). To get the most out of the supply of CCR data, there is a process you need to go through NOW – even if you do not intend to be part of the CCR regime for some months to come.

A key principle of CCR is Reciprocity – you can only access other CCR data in line with what you actually provide. To participate in CCR you need to disclose to your clients that you will be supplying data to Credit Bureaus, and you can only supply data to the Credit Bureaus from the Date of Disclosure onwards. Under the concept of Reciprocity, this therefore means that you can also only see CCR data from other sources from the Date of Disclosure onwards. For example, if you notified your clients in August 2017, you can only submit and consume CCR from August onwards – even if there is CCR data held for a client from another source dated prior to August 2017.

So how do you notify your clients?

Your Terms and Conditions on your Disclosure Documents need to advise that you are intending to share CCR data with the Bureau. An appropriate consent clause could be worded along the following lines:

"Credit agencies: In respect of us providing a credit facility and undertaking periodic reviews or for the requirements of the Anti-Money Laundering and Countering Financing Terrorism Act 2009, you authorise us to make credit references and other enquiries within our normal procedures. For this purpose, we may seek from any such source information concerning you.

You also authorise the collection and disclosure of all information relevant to your accounts including repayment history information from/to any credit reporting agency. Credit reporting agencies may use information disclosed by us to update their credit reporting database, and disclose any information that they hold about you to their own customers as permitted under the Credit Reporting Privacy Code. In addition, we may use any service provided by our credit reporting agencies to receive updates of the information it holds about you.

In the event that you are in default under any credit facility from us, we are authorised to disclose all relevant information about you, to and for the use by, credit reporting agencies, debt collection agencies and law firms."

While the above should be suitable for new clients you must also notify existing clients. As of March 2017, the legal requirement to notify your customers of your intention to move to CCR is no longer in place as long as your existing consent clause enables the sharing of CCR data. However, if your existing consent clause does not enable the sharing of CCR data, then a separate notification to your existing client is generally required.

To ensure you get the most out of your CCR experience, we suggest you you make the changes as necessary to ensure you can upload and receive as much CCR data as possible.

As always – this notice does not constitute legal advice and you should always seek independent legal advice on your specific situation.

finPOWER Connect 3.00.08 Released

Posted on Thursday, 21 September 2017

Some of the highlights are:

- Accounts.

- New, optional, "Events" block in Key Details Summary page.

- Shows recent "Events" such as Documents sent, Transactions, Logs, Audit Logs etc in chronological order.

- Applies to other Key Details Summary Pages including Account Applications and Clients.

- New Account wizard.

- New option to enter Ledger in wizard.

- Documents.

- Loan Thank You letter; updated to a "Word Document" file type.

- Deposit Certificate; updated to a "Word Document" file type.

- Deposit Tax Certificate; updated to a "Word Document" file type.

- Deposit Maturity Advice; updated to a "Word Document" file type.

- Publish Documents wizard.

- Added range for Monitor Categories.

- Security Enquiry Add-On.

- Car history.

- Option to add Sales Comparison details in HTML and PDF Reports added.

- Now supports Dealer Trade-In Valuation Price in Security Item differences grid (where Price is found).

- Electronic Signatures Add-On.

- Secured Signing.

- Now support TextLink option, i.e. send an SMS invitation to sign.

- New option for "micro" wiki text to support longer Smart Tags without wrapping details over multiple lines.

- Reports.

- Loan Trial Balance Report; optional column added for "Unearned Balance".

- Account List based Reports; now includes Grouping and Filter by Client Industry Codes.

- Fiji.

- Added support for Company Number for Clients.

- Email.

- New Verification button/ function added to Global Settings and User Preferences to test configuration.

- Auditing.

- Added auditing for Bank Accounts and Elements.

- OCR Add-On.

- OCR Add-On added (for beta testing only).

For a full list of all the release notes click here

finPOWER Connect 3.00.07 Released

Posted on Friday, 18 Auguts 2017

Some of the highlights are:

- Quick Search.

- "Open" Accounts prioritised higher.

- Loan Accounts.

- New option to complete the close process for "Closed (Pending)" Accounts in Account Processes.

- Revolving Credit Loans.

- Now support overriding dates for Interest Cycles.

- Now calculates the Loan Schedule whilst a Quote.

- Deposit Accounts.

- New Account wizard now includes a "Copy" button to copy Interest payment details to Maturity payment details.

- Logs.

- Can now be delegated to a Role, to allow all Users in that Role access.

- Documents.

- Disbursement Remittance Advice; updated to a "Word Document" file type.

- New standard Bookmarks; Last and Next Payment Date and Values.

- Workflows.

- "Create Log" Item types can now define a Delegated User and Role.

- New Automatic Outcome of "[Default]" added.

- Could not add a Workflow to a "Closed (Pending)" Account.

- Bank Account Enquiry Add-On.

- Split from Credit Enquiry Add-On, i.e. this is now a separate Add-On.

- Proviso "Bank Statements" service is now free to use.

- Added CreditSense service for New Zealand.

- CreditSense; can now define a list of Reports to display.

- Electronic Signatures Add-On.

- Docusign service added.

- Security Enquiry Add-On.

- CarHistory service added for Australia.

- Motorweb; online Vehicle Report can be used instead of the downloaded HTML Report.

- MotorWeb Security Monitoring.

- Additional range filters added to Security Monitoring wizard.

- Plate changes can now be updated from the Summary Page.

- Reports.

- Loan Aged Overdue Report; added option to include "Overdue Days" column.

- Security Item List Report; WOF and Registration dates added to data export and General filters.

- Queues.

- Added new "QueueAfterExecute" script event.

- General Ledger Interface.

- Fixed several issues with MYOB AccountRight interface.

- Auditing.

- Additional auditing options for:

- Client Branch and Manager.

- Client details for Individual, e.g. Occupation.

- Client Organisation Person Acting.

- Security Statements.

For a full list of all the release notes click here

The Finance Expo 2017

Posted on Friday, 30 June 2017

The 2017 Finance Expo is locked in for early August and has an exciting new look and feel.

This year’s edition of The Finance Expo is themed around improving the efficiency of your lending business. Hear presentations from leading industry providers, updates about the PPSR replacement programme and news on the latest trends and developments in the Finance Industry. Join us for lunch and an opportunity to interact with key industry providers.

Guest Speaker:

Also hear from Rob Bryant on how he grew a small lending business into a leading ASX listed company with over 400 employees and 70 Branches. Hear how the company did, what he learned and what he would do differently next time!

Special Deals:

Attend to receive fantastic savings from all the major sponsors – but, they will only be available on the day for those that attend.

Who should attend?

All members of the NZ finance industry are invited and the attendee list will encompass a broad spectrum of the industry, from Tier One lenders to the smallest Loan Companies.

Free Lunch?

Yes, lunch will be provided and it is free!

When and Where:

Christchurch: 2nd August, 10.30am – 2.00 pm

Sudima Hotel, 550 Memorial Ave, Christchurch Airport, Christchurch 8053

Auckland: 3rd August, 10.30am – 2.00 pm

Ellerslie Racecourse, 80 Ascot Ave, Remuera, Auckland 1051

finPOWER Connect 3.00.02 Released

Posted on Friday, 7 October 2016

Some of the highlights are:

- Accounts.

- Payment Arrangements; additional Direct Debit payment on same date not being processed correctly.

- Security Statements

- Land Security Items; now allow Prior Ranking to be greater than item's Total Value.

- Workflows.

- Australian PPSR Search implemented for Client Workflows.

- Banking

- New "BSP Biller" import service added for Fiji.

- Credit Bureaus

- Veda Australia; new product "Business Enquiry".

- Veda Australia; new product "IDMatrix" for individual verification. Note, this product is in (BETA).

- Credit Sense; updated to version 1.2 specification, including Decision Points and Supplemental Report 10.

- Centrix "Consumer Product Enquiry".

- Centrix Security Enquiry Report; updated to Summary Page 2

- NZ Companies Office; updated default URLs.

- Added Export Credit Reporting wizard.

- Electronic Signatures

- Secured Signing; new "Sign Up" button.

- Documents

- Loan Declaration of Purpose (NZ CCCFA); updated to a "Word Document" file type.

- Account Settlement Summary; updated to a "Word Document" file type.

- Reports

- Loan Cash Flow Report; added option to show outstanding Overdue as paid today.

- Security Statement Details Report; new option to include full Security Item details.

- Users

- User Policies; new option to make User Email mandatory.

- SQL Server databases

- Now allows Port Number to be specified

For a full list of all the release notes click here

finPOWER Connect 3.00.01 Released

Posted on Wednesday, 10 August 2016

Some of the highlights are:

- Accounts.

- New option to show/ hide "zero value" Interest Transactions.

- Deposits.

- Interest Payments for the same "Main" Client may now be combined.

- The final Interest Payment for a Fixed Term Deposit can now be compounded.

- Tax Certificates are now available in Australia.

- Australian PPSR.

- An issue discharging a Security Item has been fixed.

- Credit Enquiries.

- Centrix New Zealand. Added SmartID AML/CFT identity verification option to the "Consumer Product Enquiry" Credit Enquiry.

- VedaConnect Australia.: Global Settings for VedaXML and VedaConnect have been combined into one page.

- New Credit Enquiry product "Company Enquiry" has been added for VedaConnect.

- VedaXML service now warns the User that it is obsolete and to use the VedaConnect service.

- Bank Export.

- "HSBC Batch Payments" Direct Credit and Direct Debit file export added.

- General Ledger Interfaces.

- Export added for "MYOB AccountRight".

- Comprehensive Credit Reporting (BETA).

- Beta release of the new Add-On for Comprehensive Credit Reporting in Australia and New Zealand.

- Electronic Signatures (BETA).

- Added "Secured Signing" service.

- Added "Adobe Sign" service, replaces Adobe eSign service.

For a full list of all the release notes click here

finPOWER Connect 3.00.00 Released

Posted on Wednesday, 6 July 2016

This is a major release, including updated database, user interface and many new features. Please take your time reviewing the changes before upgrading.

Note, version 3 of finPOWER Connect can run side by side with version 2.x, i.e. you don't have to uninstall version 2.x.

Some of the highlights are:

- User Interface enhancements.

- Record Bookmarking added.

- Quick Search Summary; now includes Log, Email and SMS actions.

- Email Address and Phone Numbers; validation of email and phone numbers added.

- Supported Countries.

- Added support for United States of America.

- Time Zones.

- Time Zone support added.

- Account Applications.

- Now in General Release.

- Accounts.

- Standard Transactions now support a Value Basis of "Percent of Regular Payment".

- Accounting Ledgers now include a new "Suspended" Status.

- Documents.

- Word and Excel Template Document may now be embedded into the Document record.

- New "Word Document" document type.

- Does not require Microsoft Word.

- Much faster to create a document.

- Create PDF files.

- New Print Documents wizard.

- Banking.

- Direct Debits now support combining Transactions for the same main Client, Bank Account etc.

- New "CBA CommBiz Priority Payments" service added for Australia.

- Email Address and Phone Numbers; validation of email and phone numbers added.

- Credit Bureau.

- Added Centrix NZ Consumer Address Trace facility.

- Added Centrix NZ Consumer Monitoring facility.

- Centrix now support retrieving existing Reports (where available).

- NZ Companies Office interface updated to version 3 specification.

- User Interface enhancements.

- Record Bookmarking added.

- Quick Search Summary; now includes Log, Email and SMS actions.

- Email Address and Phone Numbers; validation of email and phone numbers added.

- Securities.

- Insurance Company can now link to External Party Insurers.

- Quick Search Summary; now includes Log, Email and SMS actions.

- Email Address and Phone Numbers; validation of email and phone numbers added.

- Security Enquiries.

- MotorWeb; Sign-up link and Product Names updated.

- Centrix Wheels; now includes COF status fields.

- Email Address and Phone Numbers; validation of email and phone numbers added.

- Scripting.

- Additional Code Snippets added.

- Performance optimisations.

- Email Address and Phone Numbers; validation of email and phone numbers added.

- Performance.

- New "Preload information when opening database" option added.

- Large Scripts now compile much faster.

- New Database indexes to speed up some queries.

First mobile traders sentenced under new laws with increased penalties

Posted on Thursday, 16 June 2016

The Commerce Commission have advised that mobile traders Goodring Company Limited (Goodring) and Betterlife Corporation Limited (Betterlife) have been fined a total of $171,500 after being sentenced in Auckland District Court.

They are the first to be sentenced under strengthened Credit Contracts and Consumer Finance Act 2003 (CCCFA) laws for lenders which came into force last year.

Goodring was fined $98,000 for breaches of the CCCFA, and the Financial Service Providers (Registration and Dispute Resolution) Act (FSPA). Betterlife was fined $73,500 for breaches of sections 17 and 32 of the CCCFA.

Goodring and Betterlife had earlier pleaded guilty to 28 charges and six charges respectively under the CCCFA, relating to their lending practices. Both companies failed to provide borrowers with the legally required information and the information was also not provided in a clear and concise way, as required by the Act. Goodring faced two additional charges under the FSPA. Under that Act, lenders must be registered on the Financial Service Providers register. Despite being aware of this requirement, Goodring was not registered.

For more, read here

Google Bans Payday Lender Adverts

Posted on May 12, 2016

Google has announced it will ban all payday loan ads from its site, bowing to concerns by critics who say the lending practice exploits the poor and vulnerable by offering them immediate cash that must be paid back under sky-high interest rates.

The decision is the first time Google has announced a global ban on ads for a broad category of financial products. To this point, the search giant has prohibited ads for largely illicit activities such as selling guns, explosives and drugs, and limited those that are sexually explicit or graphic in nature, for example. Critics of payday lenders say they hope the move by Google and other tech companies might undercut the business which finds huge numbers of willing customers on the internet.

The move also shows the willingness of big tech companies to weigh in on critical policy issues - and exert their power as the gateways for the internet. Facebook also does not display ads for payday loans. But others, such as Yahoo, still do.

Consumers will still be able to find payday lenders from a Google search. But the ads that appear on the top and right-hand side of a search results page will not show marketing from the payday lending industry beginning on July 13.

For more, read here

Lenders must repay all fees and interest if they don’t comply with disclosure rules

Posted on May 09, 2016

The Commerce Commission is reminding lenders that failing to disclose key information to borrowers in their consumer credit contracts could result in the repayment of all fees and interest on each loan for the period until disclosure is corrected.

Changes made to New Zealand’s credit laws (Credit Contracts and Consumer Finance Act 2003 (CCCFA)) in June last year mean lenders must disclose specific key information to borrowers, including the term of the loan, total amount, interest, fees, any security taken and the effect of that security, and the borrower’s right to apply for relief on grounds of unforeseen hardship. The Commission has been active in enforcing the law changes and currently has a number of investigations underway involving lenders that have not complied with their disclosure obligations.

Commissioner Anna Rawlings says the consequences for lenders of failing to disclose key information to borrowers are significant. “If that key information is not adequately disclosed, lenders are unable to enforce any interest or credit fees during the period of non-compliance. For some lenders this could run into the millions of dollars.”

“The law applies to lenders of all sizes and types, from small payday lenders through to our major banks. The responsibility to ensure contracts comply with the law rests squarely with those lenders and it is essential that they ensure their disclosure documents have been reviewed and they are satisfied that the documents contain all of the relevant key information required by the CCCFA,” said Ms Rawlings.

“If a lender finds their documents don’t contain all the key information they should seek legal advice immediately. We would recommend that they update the documents and disclose the missing information to all their current debtors as soon as possible.”

“Lenders had 12 months prior to the law changing to get up to speed with the changes and to ensure that their documents and processes complied with the law. Detailed information on the changes has been available to lenders and the Commission ran a number of workshops to help lenders to understand what is required of them. There is no excuse for non-compliance and the Commission will take enforcement action against those who do not comply.”

In addition to refunding the interest and fees, lenders who don’t comply with the rules could face a range of potential criminal enforcement action and fines with a maximum fine for complete non-disclosure of up to $600,000.

For more information see here

NZ Commerce Commission releases Animations to up-skill Borrowers

Posted on March 08, 2016

The Commerce Commission has today launched an original animated series to raise awareness of consumer rights. It’s All Good features New Zealand’s sharpest legal advisor Aunty and her nephew Herman Faleafa, with their debut appearance targeted at raising awareness of borrowers’ rights following the introduction of new credit laws in 2015.

The development of an animated series is a first for the Commission as part of its role to provide information and guidance about the laws it enforces, including the Credit Contracts and Consumer Finance Act (CCCFA).

Commissioner Anna Rawlings said the decision to launch the series on credit issues reflects the Commission’s focus on the consumer protection objectives emphasised in the recent credit law changes.

“Credit is widely utilised in New Zealand. It is important that borrowers understand the new processes that lenders must follow when providing credit and are familiar with their rights and obligations if they decide to get a loan,” Ms Rawlings said.

“Last year we put a considerable amount of time and effort into holding workshops with lenders to make sure they understood and would comply with the new credit laws. We also held seminars with budget advisers and community law groups to understand the key credit issues facing borrowers, and have updated our range of detailed written guidance for both borrowers and lenders.

“Developing an animations campaign reflects the diversity of the audience we need to reach and the reality that to do so requires a platform that is accessible and engaging. It’s All Good communicates serious messages in an entertaining format, providing another tool to reach consumers.”

The Commission has worked with creative advisors Stun and the Ministry for Pacific Peoples to develop the It’s All Good concept. Each episode features a situation many New Zealanders will be in at some stage in their life, for example getting a loan, being a guarantor or facing repossession.

“Over the next six weeks we will be promoting the series on social media and through our networks at budget advice and community law centres, with support from other government agencies. We also plan to tackle other issues, such as product safety and fair trading, introducing other characters into this world as it develops over the next year,” Ms Rawlings said.

finPOWER Connect 2.03.03 Released

Posted on February 03, 2016

To upgrade to this latest version please contact Amtrax Ltd, as an authorised Intersoft Reseller

Some of the highlights are:

- Clients.

- Identification Items now include an "Active" flag to deactivate an item without deleting it.

- Client Ranges now support "Main" and "All Owners" in some places, e.g. Process Direct Debit Payments wizard.

- Accounts

- New option for Loan Accounts to apply a Minimum and Maximum Net Advance limit.

- New Account wizard; new option to default Residual Value from Net Advance.

- Email and SMS "to" lists now include the Dealer and Broker, and associated employees, of the Account.

- Loan Statement; new option to include an Interest Rate breakdown for Interest transactions.

- Account Applications.

- Added Employment details for Individual Applicants.

- Collateral Item wizard; now includes Insurance details.

- Collateral Items; now include options to run a PPSR Search and Security Enquiry.

- Transactions.

- Transaction Entry; new option for Credit Interest to automatically post Withholding Tax.

- Withdrawal Bank Transactions; can now be reversed.

- Export Bank Transactions; new option for "Re-Export" to include or exclude Reversed Transactions.

- Bank Lodgement; new option for "Re-Print" to include or exclude Reversed Transactions.

- Income Distribution; new option to edit values and to save as a Transaction batch.

- Disbursements.

- Enhanced messages when reversing Disbursements.

- Approving, Cancelling and Reversing Disbursements, new scripting functions added.

- Workflows.

- New Item Types "Account Restructure" and "Security Enquiry."

- Security Register Search" Item Type now supports Australian PPSR.

- Bank Account Enquiry items now send Email/ SMS in unattended mode if possible.

- Tax Certificates.

- Implemented for Fiji and Papua New Guinea.

- General Ledger Export.

- New option to default the GL Export Id.

- Addressing.

- Added "United States of America" as a supported Country.

- Page Sets.

- Grid Rows can now be hidden.

- Centrix.

- Security Enquiry now includes "Confirm Owner" enquiry.

- Veda Connect Australia.

- "Vedascore Apply" Credit Enquiries have been updated to the latest specification.

- Electronic Signatures.

- Downloaded documents are now automatically saved to the Account, Client etc document folder.

- Code Snippets.

- New code snippet samples added.

- Window tabs.

- Can now be dragged to re-order.

finPOWER Connect Newsletter

Posted on December 23, 2015

The Commerce Commission has prosecuted Sunway Finance Limited

As a follow up to our previous article here, the Commerce Commission has now successfully prosecuted Sunway Finance Limited (Sunway).

Sunway, an unlicensed money lender, was fined $30,000.00 in Auckland District Court and all of its loan contracts were extinguished. As a consequence, debtors do not have to pay back any outstanding money under these loans.